Private banks doing well

![]()

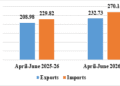

India’s exports could face headwinds in the event of sustained global slowdown as has been witnessed so far, said the Reserve Bank of India (RBI) in its Economic Outlook for 2020.

Reviving the twin engines of consumption and investment while being vigilant about spillovers from global financial markets remains a critical challenge going forward, it said in a report on 27 Dec 2019.

Scheduled commercial banks’ (SCBs) credit growth remained subdued at 8.7% year-on-year (y-o-y) in September 2019, though Private Sector Banks (PVBs) registered double digit credit growth of 16.5%.

SCBs’ capital adequacy ratio improved significantly after the Government recapitalized public sector banks (PSBs).

SCBs’ gross non-performing assets (GNPA) ratio remained unchanged at 9.3% between March and September 2019.

Provision Coverage Ratio (PCR) of all SCBs rose to 61.5% in September 2019 from 60.5% in March 2019 implying increased resilience of the banking sector.

Macro-stress tests for credit risk show that under the baseline scenario, SCBs’ GNPA ratio may increase from 9.3% in September 2019 to 9.9% by September 2020 primarily due to change in macroeconomic scenario, marginal increase in slippages and the denominator effect of declining credit growth.

As per network analysis, total bilateral exposures between entities in the financial system registered a marginal decline in quarter ended September 2019.

Among all the intermediaries, Private Sector Banks (PVBs) saw the highest y-o-y growth in their payables to the financial system, while insurance companies recorded the highest y-o-y growth in their receivables from the financial system.

Commercial Paper (CP) funding amongst the financial intermediaries continued to decline in the last four quarters.

The size of the inter-bank market continued to shrink with inter-bank assets amounting to less than 4% of the total banking sector assets as at end-September 2019.

This reduction, along with better capitalisation of PSBs led to a reduction in contagion losses to the banking system compared to March 2019 under various scenarios relating to idiosyncratic failure of a bank, non-banking finance company (NBFC), housing finance company (HFC) and macroeconomic distress.

RBI has initiated policy measures: to introduce a liquidity management regime for NBFCs; to improve the banks’ governance culture; for resolution of stressed assets and for the development of payment infrastructure.

It has also accepted some of the key recommendations of the Task Force on Offshore Rupee Markets viz., allowing domestic banks to freely offer foreign exchange prices to non-residents and allowing rupee derivatives (with settlement in foreign currency) to be traded in International Financial Services Centres (IFSCs).

The Securities and Exchange Board of India (SEBI) has taken a number of steps to improve the financial markets including a revised risk management framework of liquid funds, revised norms for investment and valuation of money market and debt securities by mutual funds (MFs), revised norms for credit rating agencies (CRAs), facilitating new commodity derivative products and setting up institutional trading platforms (ITPs) on stock exchanges to promote start-ups.

The Insolvency and Bankruptcy Board of India (IBBI) continues to make steady progress in the resolution of stressed assets.

The Insurance Regulatory and Development Authority of India (IRDAI) has taken initiatives for growth of InsurTech and strengthening insurers’ corporate governance processes.

The Pension Fund Regulatory and Development Authority (PFRDA) continues to bring more citizens under the pension net, said RBI. fiinews.com